OEM Self-Developed Chips Reshape Auto Supply Chain: BYD, NIO, XPeng Challenge Third-Party Suppliers

OEM Self-Developed Chips Reshape Auto Supply Chain: BYD, NIO, XPeng Challenge Third-Party Suppliers At least five major automakers are now developing their own autonomous driving chips, signaling a tectonic shift in the automotive supply chain that threatens to upend the dominance of third-party chip suppliers. BYD, NIO, XPeng, Li Auto, and Tesla have all introduced or announced in-house chips, each claiming performance metrics that rival or surpass commercially available sol

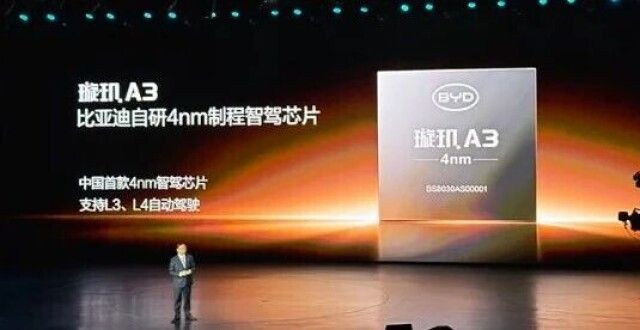

OEM Self-Developed Chips Reshape Auto Supply Chain: BYD, NIO, XPeng Challenge Third-Party Suppliers At least five major automakers are now developing their own autonomous driving chips, signaling a tectonic shift in the automotive supply chain that threatens to upend the dominance of third-party chip suppliers. BYD, NIO, XPeng, Li Auto, and Tesla have all introduced or announced in-house chips, each claiming performance metrics that rival or surpass commercially available solutions. BYD's Xuanji A3 chip, built on a 4nm process with 700 TOPS of computing power, entered mass production in May 2026. XPeng's Turing chip, delivering 750 TOPS, began production in the third quarter of 2025 with an annual output of approximately 1 million units. NIO's Shenji NX9031, fabricated on a 5nm process and exceeding 1,000 TOPS, has already shipped 150,000 units. Li Auto's Mach M100, also on 5nm, claims 1,280 TOPS of "effective compute." Tesla's HW4 rounds out the competitive landscape. The impact on third-party suppliers has been immediate. Horizon Robotics, a leading Chinese autonomous driving chip company, saw its stock drop 7 percent following BYD's chip announcement. The decline is significant because BYD is Horizon's largest customer, accounting for roughly 50 percent of its revenue. When a dominant customer becomes a competitor, the business model faces existential risk. However, Horizon Robotics maintains substantial defensive moats. The company's toolchain maturity is widely recognized as best-in-class, with 27 original equipment manufacturers (OEMs) and 42 brands integrated into its ecosystem. Horizon is also expanding its product line with the Star series, a cockpit-driving fusion chip that combines infotainment and autonomous driving capabilities in a single SoC — an area where most OEM chips have yet to compete. The supply chain disruption extends beyond chipmakers to Tier 1 suppliers, who are being squeezed as OEMs take back system-level control over electronic architectures. In the short term, spanning 2026 to 2027, OEM-developed chips will likely remain confined to high-end models, leaving basic third-party chip business largely unaffected. The medium-term outlook from 2027 to 2028 becomes critical: if OEM chips successfully penetrate sub-200,000 RMB models at million-unit scale, the competitive dynamics shift decisively. Looking further ahead, if in-house chip capability becomes a core competitive barrier for OEMs, third-party chip companies face systemic customer base shrinkage. For an industry built on the horizontal division of labor between automakers and suppliers, the vertical integration trend represents the most profound restructuring in a generation. The question is no longer whether OEMs can build chips, but what role remains for those who only sell them.

📌 Kaynak

Bu özet Pandaily kaynağından otomatik derlenmiştir. Tamamı için orijinal habere gidin.

Orijinal haberi oku →